2021 is one of the hottest years to be a VC – or a startup. Regionally, globally… Plenty of investment rounds, exits, new SPACs… so the returns shouldn’t be any different than sky-high, right? Well, that’s what I’ve researched this month…

Who’s gonna return the fund?

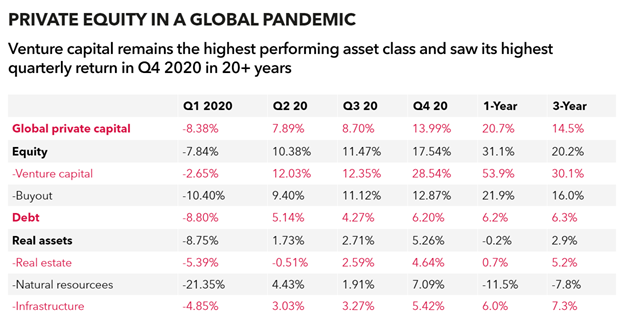

This year looks so good in terms of the VC investment raised. How about the VC returns though? Globally, venture capital was the top performing asset class when it comes to PE/VC funds in 2020. In general, though, it’s not easy to access the individual data to begin with. A few may reach up to 700% (7x committed capital), many would be negative.

Globally, venture capital returned 28.5% in Q42020 ― the highest return since the dotcom era, and the 1-year IRR of VC funds surpassed 53% (vs. 19% in 2019).

Source: Burgiss; Q4 2020 Global Private Capital Review

The best VC times to live in?

If you’ve been investing for the past 5-10 years, your investments are currently maturing, and the returns are touching the sky for few. The lucky investors indeed got a well-diversified portfolio and apply Pareto wherever they go: 80% of good returns come from 20% of your investments. So, as the principle goes, out of 10 startups you invested in, 1 will really explode and IPO/M&A and another 1 will get you medium returns. These 2 stars will basically “return the fund” (and make the LPs very happy). In general (not always the case) LPs are happy when they get a 3x or more return of committed capital, e.g. a $100 million fund will generate a $300 million return. That’s ideal. (The 3x return gets trickier to achieve the bigger your fund size is.)

The returns of course depend on the stage. Seed fund returns are riskier but, if positive, they are much more ravishing than other types of VC funds. Seed-focused VCs won’t accommodate to the lower returns of later-stage funds because of the risk they bear. Put simply, seed investors shoot for ~50x or more from one investment, Series A investors eye 10x to 15x and later stage investors seek 3x to 5x.

Unicorns x returns

One of the pointers in my research was the market valuation of unicorns, which is, as of April 2021, $0.951T in Asia Pacific, $0.929T in North America, with Middle East & Africa (MEA) at the tail with only $0.021T. (Note that the MEA figure doesn’t include Swvl.)

However, the fact that we don’t have that many unicorns here doesn’t necessarily mean sluggish fund performance. With the existing MEA fund sizes, if you invested early, own a decent stake in early-stage companies and few of those companies exit at around $250M, as a fund you can make good returns. So, in reality, you don’t need to have unicorns to be labeled as a high performer. As a comparison, VCs managing more than $1B funds need to have 1 or 2 unicorns to generate good returns – however, those funds are based in more mature developed markets.

Moreover, the above data suggests there is much room for new unicorns in MEA. The record-smashing 2020 and H12021 results only confirm that the regional and international VCs investing here are willing to make higher-than-ever bets on the local startups, eyeing more than just “returning the fund”.

Variations between global VC returns

During 2010 and 2020, the venture capital was the top performer in the United States and returned an average of 15.15% per annum (while S&P 500 did 13.6% during the same period).

From 2007 till 2017, the financial performance of UK VC funds has been comparable to the US with UK performance only slightly lower than US funds of the same vintage.

PitchBook looked at 82 VC funds launched in 2010-12. They had a median average annual return of 11% during Q12020 though the very best of them returned more than 50% – those that saw plenty of exits. The worst had a negative 6%. So, the gap between the best and the worst performers is profound. Those funds that had invested in MongoDB, Etsy, Tumblr, Zoom and Uber were among the top performers.

A cherry on the cake: some of the funds with a vintage year 2019 are reportedly recording an IRR of up to 119%.

Well, I can’t really compare that to our local funds’ IRRs because such data barely exists. Some VCs say it’s confidential, others say the numbers are only estimates anyway.

Since one way to assess profitability is by analyzing the exits, we can at least check out the most interesting exits that took place this year and see who backed them:

- Anghami’s IPO – MEVP, SHUAA Capital, Samena Capital, Megladon, Endeavor, Sal&Co (+ others)

- Swvl’s IPO – Arzan Venture Capital, Beco Capital, Oman Technology Fund, Raed Ventures, Sawari Ventures (+ others)

- TreasuryXpress (UAE) – MEVP, Azure Capital Partners, The Luxury Fund (+ others)

- Spotii (UAE) – Daman Investments

- Mumzworld (UAE) – Gulf Islamic Investments, Swicorp, Wamda Captial, Global Ventures, Endeavor Catalyst, Saned Partners (+ others)

- Eventtus (Egypt) – Algebra Ventures, MEVP, Raed Ventures, 500 Startups, Cairo Angels, Daal, Hala Ventures (+ others)

- WaysToCap (Morocco) – Y Combinator, Battery Ventures, Soma Capital, Palm Drive Capital, Amino Capital, Endure Capital (+ others)

- Invoice Bazaar (UAE) – Advance Global Capital

- Ostaz by Synkers (Lebanon) – Phoenician Funds, Crescent Capital, 500 Startups, Dubai Angel Investors, Mulcan International Investments (+ others)

And, lastly, I had a look at the strongest vintage years for funds operating in the region:

- 2015―funds with 2015 vintage had invested in Careem, Souq.com, Anghami, Fresha, TruKKer…

- 2018―another great vintage. Investments included Swvl, Kitopi, MaxAB. And these funds keep on investing till now.

It would be an interesting exercise to look deeper into all the recent exits and create a mosaic of all the funds involved. Maybe another month. With 30+ exits since January 2021, there will be a lot of name-dropping.

|

TL;DR (too long; didn’t read)

Returning the fund has become possible for a greater number of funds. Globally, the returns of venture capital were the highest since the dotcom era. For now, the market valuation of unicorns in the MEA region remains very low compared to Asia Pacific and North America. Yet, the record 2020 and H12021 results suggest that the regional VCs (and international VCs) are willing to make higher-than-ever bets in the Middle East, eyeing more than just "returning the fund". The strongest vintage years for regional funds include 2015 and 2018.

|

The finalists 🌍

Our latest investment – Klaim – won the UAE round in KPMG Private Enterprise Tech Innovator 2021 competition. The finals will be at Web Summit 2021 in Lisbon, Portugal this November. We wish you the best of luck, Klaim!

1 million orders in 1 year

Within 12 months of operations, over 1 million orders have been placed on Retailo‘s app across MENAP’s region.

Onto Pakistan

In line with its expansion plans, TruKKer acquired TruckSher, one of Pakistan’s leading and most innovative digital land freight platforms.

Zid Pay

Zid launched Zid Pay to address the most urgent challenges faced by online retailers and to bridge the gap between payment providers and retailers.

Fintech innovation after covid

SubsBase was recognized by Plug and Play Tech Center as one of the “The 13 Fintech Payments Startups That Are Changing the Way We Pay”.

- Logistics Manager at Fatura (Cairo)

- Key Account Sales Manager at TruKKer (Cairo)

- DevOps Engineer at Qoyod (Cairo)

- Head of Sales & Growth at Retailo (Riyadh)

- Logistics Manager at Citron (Dubai)

Enjoy the weekend!

Hasan

![]()

![]()

![]()

![]()

![]()

![]() Received this from a kind friend? You can subscribe to our newsletter too.

Received this from a kind friend? You can subscribe to our newsletter too.

Copyright © 2021 ArzanVC, All rights reserved.

Want to change how you receive these emails?

You can update your preferences or unsubscribe from this list